We no longer support this browser. Using a supported browser will provide a better experience.

请 更新浏览器.

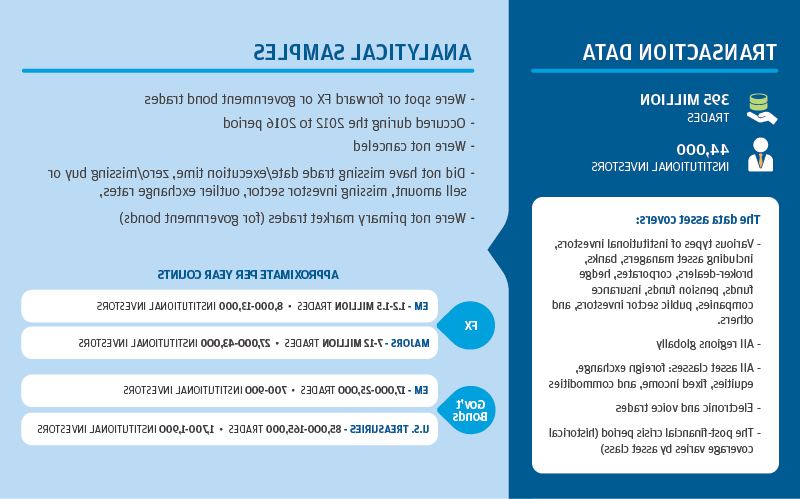

In this 澳博官方网站app 研究所 report on financial markets, 我们利用2013年中期的“缩减恐慌”事件来阐明围绕重大货币政策冲击的市场走势和机构投资者行为之间的相互作用, focusing on spillovers to emerging market (EM) currencies. 我们之所以研究“缩减恐慌”,是因为它代表了金融危机后使用大规模资产购买(LSAPs)的一个关键事件。. Given the sustained low level of interest rates over the past decade, these measures have become an indispensable part of the modern central banking policy toolkit; however, 政策制定者对市场参与者的预期和对政策调整的潜在反应并不完全了解,这意味着这些计划很难顺利解除.

Using the unique data available to the 研究所, we document how investor behavior changed starkly around the onset of the taper tantrum, as flows from market participants that on-net were buying EM currencies began to reverse. 除了, 在缩减恐慌的背景下,我们利用数据的粒度特性来帮助回答以下三个问题:

这些问题的答案, grounded in new data (summarized in the graphic below), 提供了有关“缩减恐慌”时期如何在新兴市场货币市场展开的见解,并就投资者行为在导致市场大幅波动方面的潜在作用提供了更普遍的经验教训. Accordingly, we organize our research around three findings described in the following pages. The taper tantrum represents a key episode in the post-financial crisis use of large-scale asset purchases.

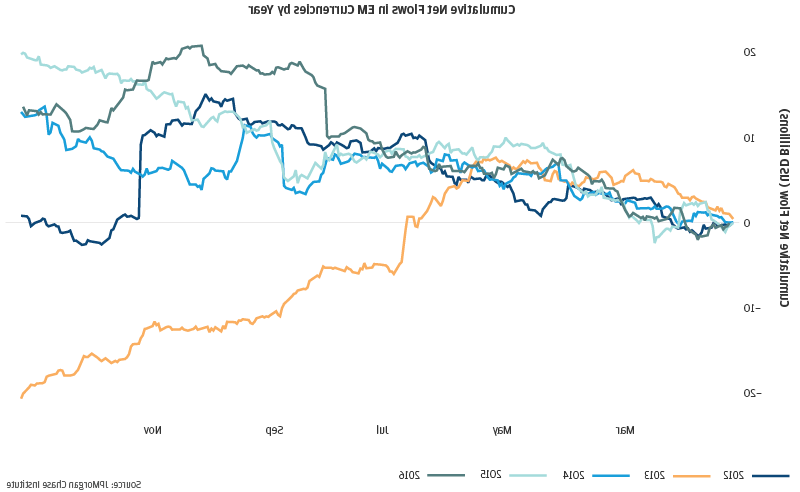

Over the post-crisis period we study, 我们在投资者部门层面分解的净流量数据,可以解释新兴市场外汇和政府债券市场变化的很大一部分. 将净流量纳入这些新兴市场资产的回归中,解释力(r平方)的提升幅度从25%到50%以上, 视情况而定, relative to the combined forecasting ability of U.S. 股票和国债收益率. 关注新兴市场货币, 哪里的数据更好, we also find time variation in the relationship between net flows and EM currency index changes. 特别是, 在流动性较低的情况下,资产管理公司对新兴市场货币的抛售会导致比正常情况大得多的贬值. 我们在2013年5月的数据中看到的总资金流急剧逆转——与“缩减恐慌”(taper tantrum)的开始密切相关——表明,市场参与者交易在这一时期对贬值程度起到了一定作用.

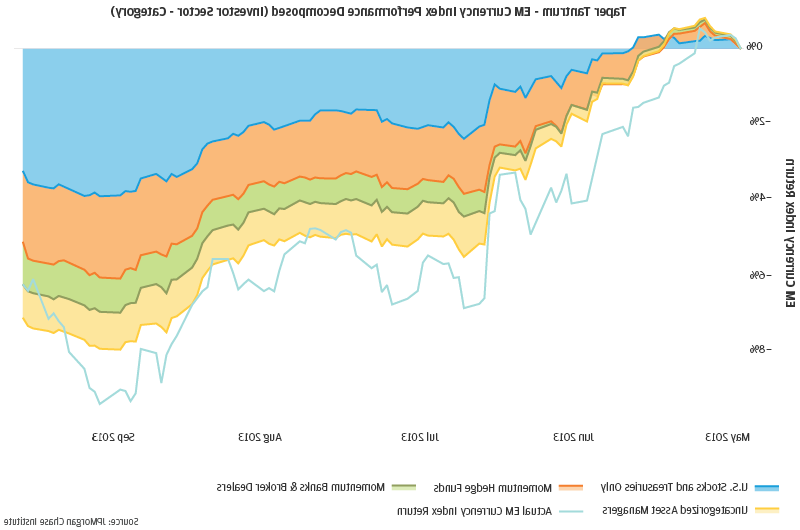

To supplement our sector-level flows, 我们根据易于观察到的交易系统模式对市场参与者进行分析,以了解某些部门的流动与市场运动之间明显的密切联系的本质. 在一个关键结果中, we identify relatively small pockets of the investor base—namely, 对冲基金和银行与动量交易有关,它们似乎推动了净流量的解释力. 此外, 资产管理公司的交易通常不会表现出强烈的系统性模式,但在“缩减恐慌”期间,这些交易改变了它们的行为,并与新兴市场货币贬值高度相关. 看看这三个投资者群体在缩减恐慌期间是如何影响价格走势的, 我们使用新导出的投资者原型(使用样本外数据分类)对新兴市场货币2013年的表现进行了回归. 如下图所示, 来自这些市场参与者的资金对价格走势的预测贡献与市场动态很好地吻合,并且可以在很大程度上解释累积的“缩减恐慌”(taper tantrum)贬值,其幅度超出了美国央行的预测.S. 市场走势本身.

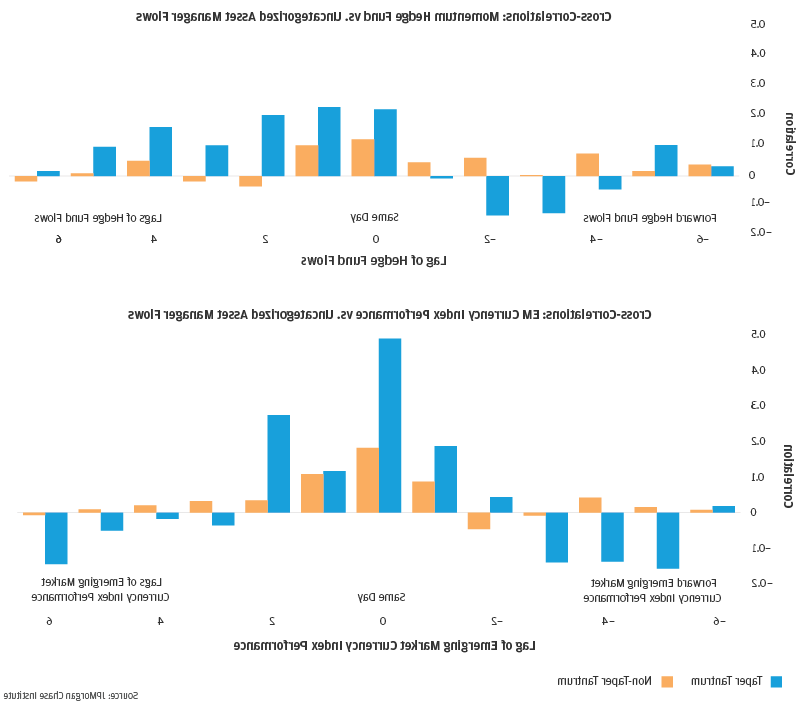

在缩减恐慌期间, 很大一部分资产管理公司的交易与其他投资者类别和同期价格走势变得更加高度相关. 另外, 我们发现,有证据表明,资产管理公司追踪与动量相关的对冲基金的流动时存在几天的滞后, suggesting a leader-follower dynamic that does not typically appear. To illustrate more closely the temporal dimension of these relationships, 我们(在下图中)绘制了资产管理公司与对冲基金流动和价格行为之间的相关性,其中包含各种领先和滞后. A few observations stand out: first, the transactions of asset managers tracked lagged hedge fund flows but not the other way around; and second, 在“缩减恐慌”期间,同期的流量-流量和流量-价格相关性明显高于平时(我们测试了这不仅仅是插曲期间波动性变化的函数)。.

最后, 在“缩减恐慌”期间,新兴市场货币贬值的关键闪点与我们数据中新兴市场货币买家与卖家数量的急剧(负)异常值有关, which further points to herding activity that potentially affected market dynamics.

澳博官方网站app & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. 请 review its website terms, privacy and security policies to see how they apply to you. 澳博官方网站app & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the 澳博官方网站app & Co.