我们不再支持这个浏览器. 使用受支持的浏览器将提供更好的体验.

请 更新浏览器.

The 新型冠状病毒肺炎。 pandemic resulted in an unprecedented recession that impacted families’ financial positions. The 澳博官方网站app 研究所 leverages de-identified administrative banking data to assess checking account balances in conjunction with household income and spending. 基于最近的JPMC研究所 研究, this Household Finances Pulse analyzes changes in cash balances during the 新型冠状病毒肺炎。 pandemic and ongoing recovery across the distribution of cash balances and by income quartile.

大流行期间, the federal government provided cash assistance directly to families through stimulus payments, 失业保险, 最近, 高级儿童税收抵免(CTC). 第一轮经济刺激, 或经济影响支付(EIP), 4月15日开始, 2020年,交付高达1美元,每位成人200美元,每位符合条件的儿童500美元. 第二轮EIP于2021年1月分发, providing up to $600 per eligible adult or child The third round of stimulus was paid out beginning March 17, 2021, 提供1美元,每位符合资格的成人或儿童400英镑. 在此期间, 扩大失业保险,为失业人员提供支付, 包括零工和个体经营者, 在2020年3月至7月期间,每周可获得600美元的补贴, 从2020年10月到2021年1月,每周补贴300美元. Twenty-six states phased such expansions in both eligibility and payment supplements in June and July 2021. 7月15日, 2021, 发放了第一笔每月预付儿童税收抵免, paying up to $300 per child under 6 years of age and up to $250 per child aged 6 to 17 years.

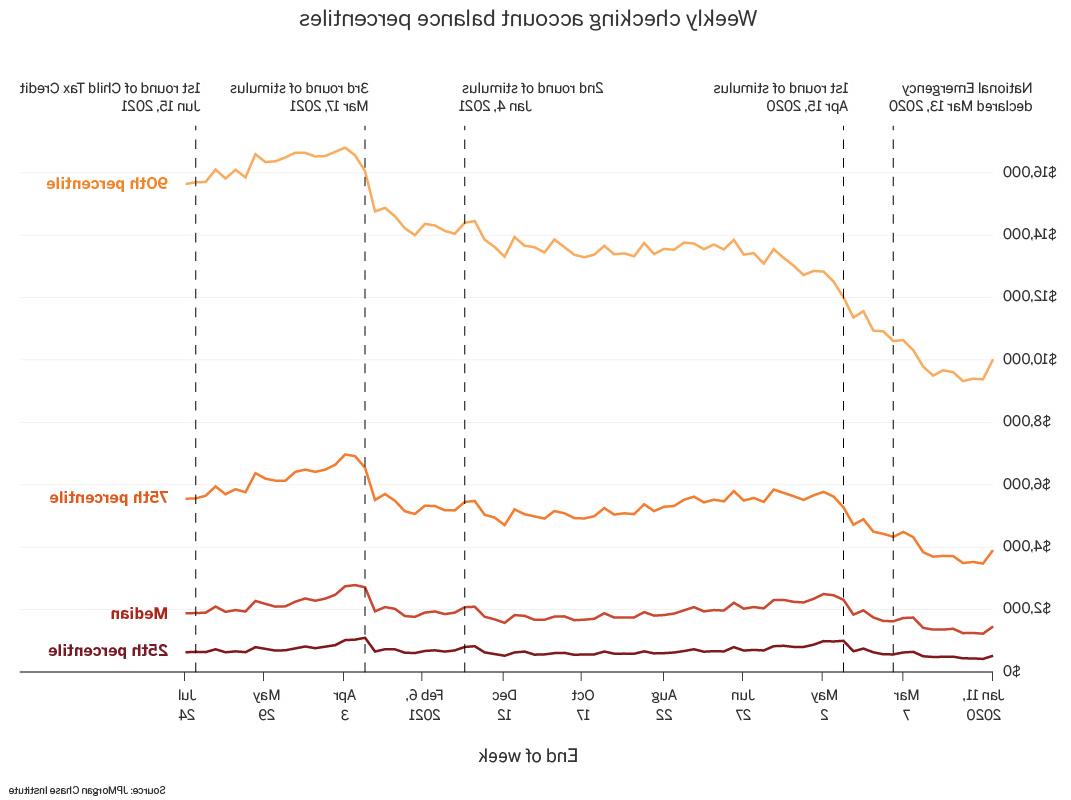

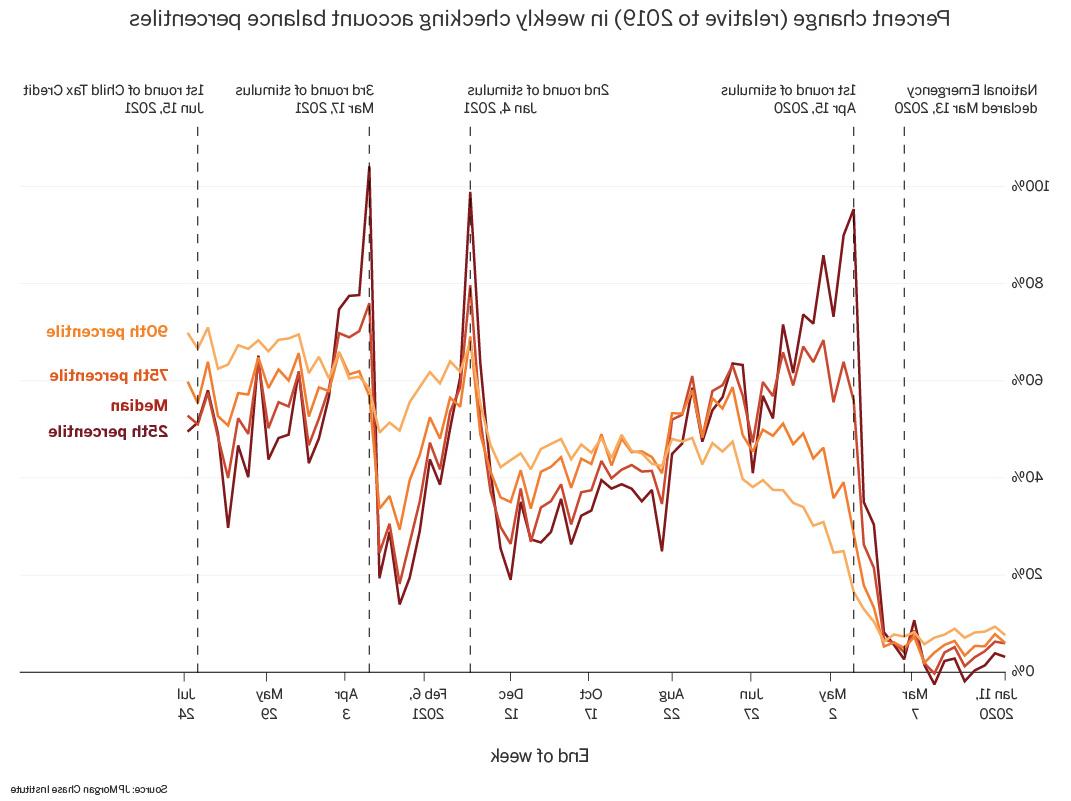

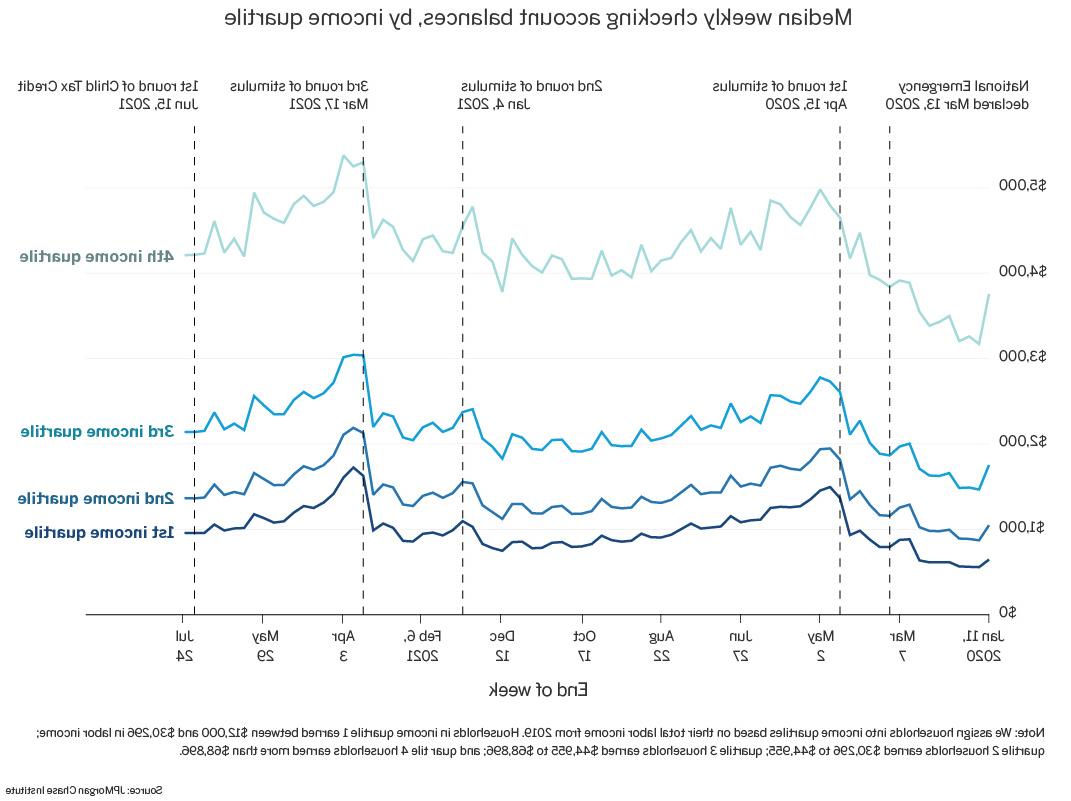

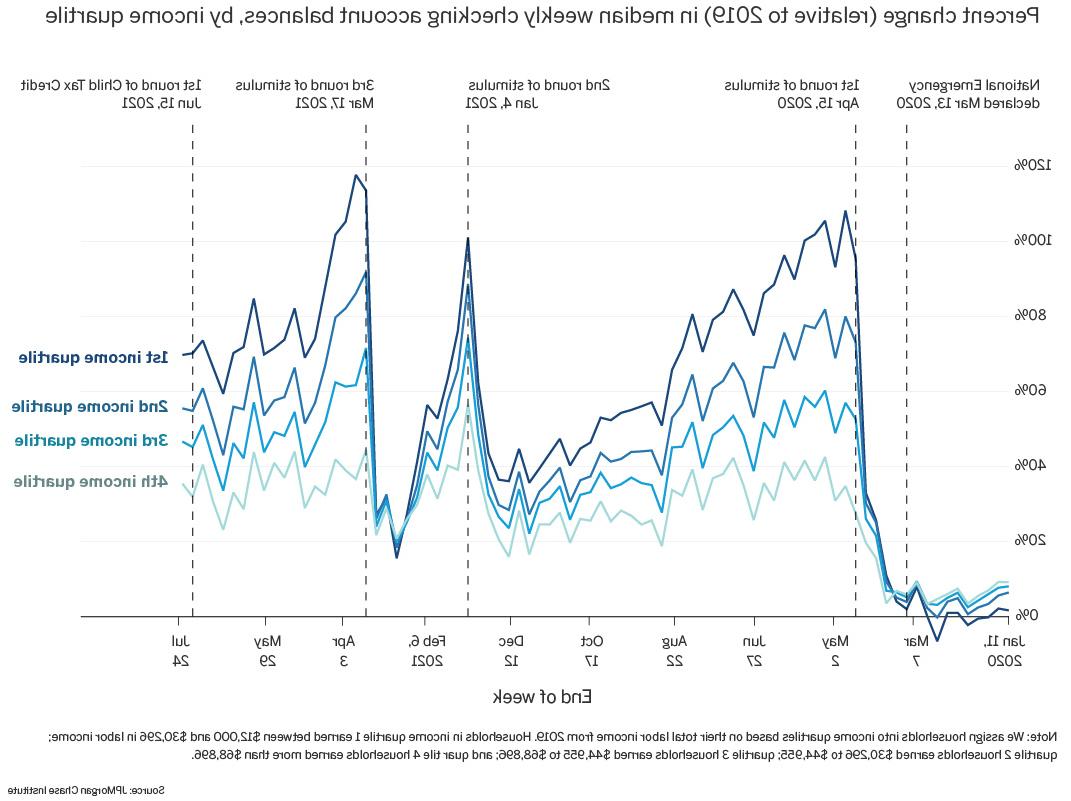

Median cash balances are more than 50 percent higher as of the end of July 2021 compared to the same period in 2019. 如图1和图2所示,我们观察到在90中增加了更大的百分比th 余额的百分位数, 暗示经济持续增长, 特别是在流动资产分配的顶端. 除了, Figures 3 and 4 reveal that the balances of lower-income families (income quartile 1) are roughly 70 percent higher than 2019 levels, while higher-income families (income quartile 4) have balances roughly 35 percent higher than 2019 levels.

在每一轮刺激之后, the low end of the liquid assets distribution and families with low incomes experienced larger proportional increases in balances but also faster depletion of those balance gains in the weeks after the stimulus, 显示针对性支持的重要性. Figures 1 and 3 show that the third round of stimulus was much larger in magnitude than the second round of stimulus, 而且当时现金余额已经很高了. 可能的结果是, the balance gains from round three appear to be depleting more slowly than those from round two (Figures 2 and 4).

考虑到它的规模和覆盖范围比刺激支出要小, the Advanced Child Tax Credits did not result in a large cash boost seen with each round of stimulus. 也就是说, the Advanced CTC is a monthly payment that may be slowing the depletion of balance gains from the third stimulus, 从而在COVID大流行期间支持家庭现金缓冲. The aggregate magnitude of the Advanced Child tax credit payment is small relative to the other forms of government cash assistance discussed above. 根据 财政部的声明,联邦政府支付了12美元.到2021年7月,提前儿童税收抵免将达到70亿美元,而此前为28亿美元.失业救济在同一个月减少了30亿美元(和39亿美元).到2021年6月,将达到10亿美元) 超过4000亿美元 在第三轮经济影响支付中. 换句话说, Advanced CTC was roughly half the size of federal UI payments in July and just 3 percent of the magnitude of the third round of stimulus.

These aggregate values are smaller in part because the share of families receiving the payment is smaller—roughly 35 million households with children, 占美国1.28亿家庭总数的27%.S.收到付款. 相比之下, 大约85% 的成年人收到了刺激支票. 除了, the magnitude of the payment per family is smaller for the Advanced CTC than for any of the three rounds of stimulus. 重要的是, leading up to the arrival of the Advanced CTC payment cash balances of families are falling. 因此, Advanced CTC may be helping to slow the spend down of cash balances after the third round of stimulus.

图1:现金余额随着每一轮刺激的到来而增加, 并且相对于大流行前的水平仍处于较高水平

图2:现金余额随着每一轮刺激的到来而增加, 在分布的低端有较大的百分比增长

图3:所有收入水平的家庭, 现金余额随着每一轮刺激政策的出台而增加, 并且相对于大流行前的水平仍处于较高水平

图4: 伴随着每一轮的刺激, 低收入家庭的现金余额增幅最大, 但这些收入消耗得比高收入家庭快

We thank our internal partners for his their support, specifically Anthony Rivera. 我们感谢我们的内部合作伙伴和同事, 谁以各种方式支持我们的议程, 并感谢他们对每个和所有版本的贡献.

我们要感谢澳博官方网站app的首席执行官杰米·戴蒙 & Co., for his vision and leadership in establishing the 研究所 and enabling the ongoing 研究 agenda. 我们仍然深深地感谢彼得·谢尔, 副主席, 德米特里Marantis, 企业责任主管, 希瑟Higginbottom, 研究主管 & 政策, and others across the firm for the resources and support to pioneer a new approach to contribute to global economic analysis and insight.

This material is a product of 澳博官方网站app 研究所 and is provided to you solely for general information purposes. 除非另有特别说明, any views or opinions expressed herein are solely those of the authors listed and may differ from the views and opinions expressed by J.P. 摩根 Securities LLC (JPMS) 研究 Department or other departments or divisions of 澳博官方网站app & Co. 或者它的附属机构. 本材料不是JPMS研究部门的产品. Information has been obtained from sources believed to be reliable, but 澳博官方网站app & Co. 或其联属公司及/或附属公司(统称为J.P. 摩根)不保证其完整性或准确性. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. The data relied on for this report are based on past transactions and may not be indicative of future results. The opinion herein should not be construed as an individual recommendation for any particular client and is not intended as recommendations of particular securities, 金融工具, 或者针对特定客户的策略. This material does not constitute a solicitation or offer in any jurisdiction where such a solicitation is unlawful.

澳博官方网站app & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. 请 review its website terms, privacy and security policies to see how they apply to you. 澳博官方网站app & Co. 不负责(也不提供)任何产品, 该第三方网站或应用程序的服务或内容, 明确带有澳博官方网站app字样的产品和服务除外 & Co.